[Click here for a standalone PDF of this post]

Motivation

The banks are all offering variable rate mortgages at slight differences from prime (current 3%). I have asked for a few competing rate quotes to see which is best.

Scotiabank offered \(\text{prime} – 0.53\%\). PC Financial offered \(\text{prime} – 0.55\%\), slightly better. ING’s offer wasn’t competitive at \(\text{prime} – 0.25\%\). BMO offered the best so far at \(\text{prime} – 0.6\%\), with the conditions that we’d have to open joint chequing and a joint BMO mastercard. Royal’s default offering matched PC Financial’s offer at \(\text{prime} – 0.55\%\), and she’s now playing the back room manager game to see if she can get approval to beat (or even match) BMO’s offer.

Let’s compare those here and see how much difference these quotes result in. Is it even worth it to do this negotiation?

Guts

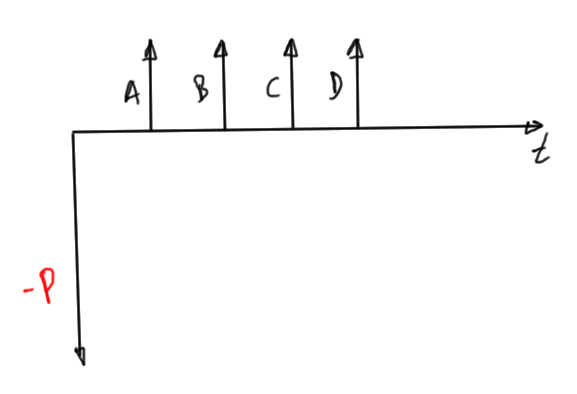

Consider first a principle amount \(-P\), and set of payments \(A, B, C, D, …\), equally spaced in time, corresponding with some effective interest rate per period. This is sketched in fig 1.1.

Fig 1.1: Payments at fixed intervals

We want to refresh our memory about future value calculations for such a set of payments. Suppose the interest rate per period is \(i\), for example \(i = 0.03\) for a 3% rate, then at the first, second, third, and fourth intervals, we have respectively

\begin{equation}\label{eqn:mortgageInterest:20}

\begin{aligned}

-P(1 + i) + A & \\

\lr{ -P(1 + i) + A }(1 + i) + B &= -P(1+i)^2 + A(1 + i) + B \\

\lr{ \lr{ -P(1 + i) + A }(1 + i) + B}(1 + i) + C &= -P(1+i)^3 + A(1 + i)^2 + B(1 + i) + C \\

\lr{ \lr{ \lr{ -P(1 + i) + A }(1 + i) + B}(1 + i) + C}(1 + i) + D

&= -P(1+i)^4 + A(1 + i)^3 + B(1 + i)^2 + C(1+i) + D.

\end{aligned}

\end{equation}

We can treat the payments independently, each with a separate \((1+i)^k\) factor adjusting the future value of that payment. The case where the payments are of equal value is of particular interest. For that, after \(k\) payments, the future value of the initial principle offset by any of the payments is

\begin{equation}\label{eqn:mortgageInterest:40}

F_k

= -P(1+i)^k + A(1 + i)^{k-1} + A(1 + i)^{k-2} + \cdots A.

\end{equation}

Recall that a geometric sum

\begin{equation}\label{eqn:mortgageInterest:60}

S_k = 1 + a + a^2 + \cdots + a^{k-1},

\end{equation}

can be solved by writing

\begin{equation}\label{eqn:mortgageInterest:80}

a S_k – S_k = a^k – 1,

\end{equation}

so that

\begin{equation}\label{eqn:mortgageInterest:100}

S_k = \frac{a^k – 1}{a – 1}.

\end{equation}

The future value thus sums to

\begin{equation}\label{eqn:mortgageInterest:120}

F_k

=

-P(1+i)^k + A \frac{ (1 + i)^k – 1}{ 1 + i – 1 },

\end{equation}

or

\begin{equation}\label{eqn:mortgageInterest:160}

\boxed{

F_k

=

\lr{ -P + \frac{A}{i} } (1 + i)^k – \frac{A}{i}.

}

\end{equation}

Observe that we can invert \ref{eqn:mortgageInterest:160} for \(k\) by taking logs of the inequality \(F_k \ge 0\). This gives

\begin{equation}\label{eqn:mortgageInterest:180}

\boxed{

k \ge – \frac{\ln\lr{ 1 – i P/A}}{\ln\lr{1 + i}}

}

\end{equation}

It’s clear that we are in trouble (with always negative future value, and no solution to the inequality) unless \(-P + A/i > 0\), or

\begin{equation}\label{eqn:mortgageInterest:140}

A > i P.

\end{equation}

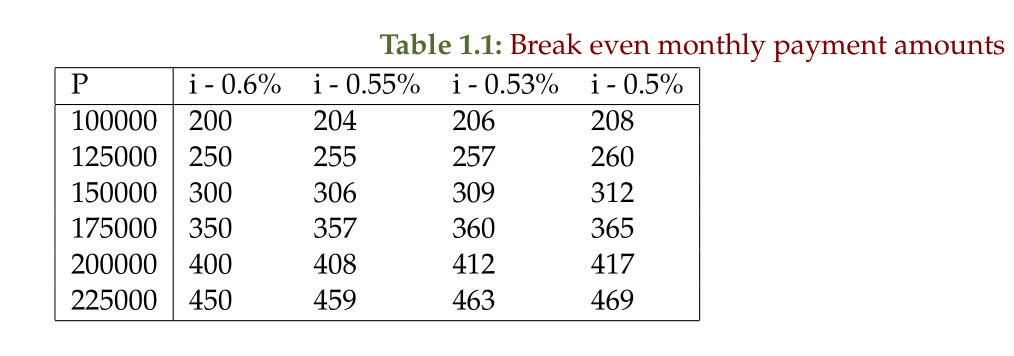

For example, at \(i = 3\%\) interest per year, compounded monthly, the monthly break even payment rate for various mortgage amounts \(P\) is tabulated in table 1.1

This provides a first hint that the 0.5-0.6 less than prime rates that the various banks offer will make a difference. For a principle of \(200 K\), we require \(17\) dollars more per month to break even (not paying down the principle at all) when comparing prime less \(0.5\%\) and \(0.6\%\).

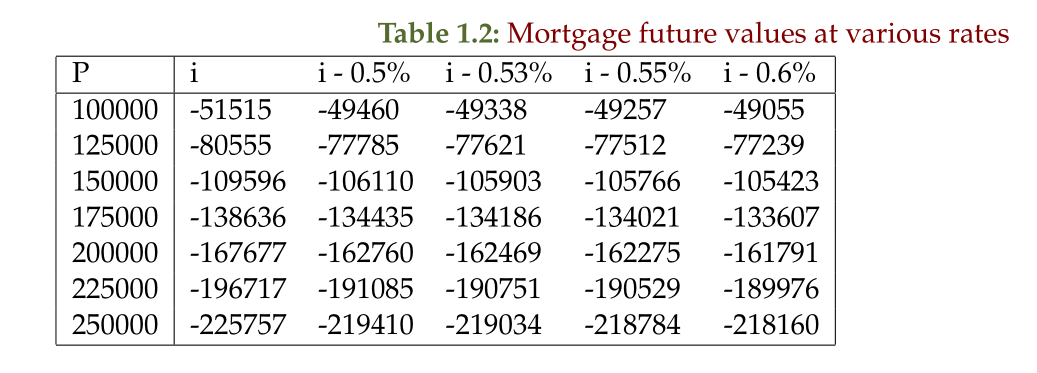

Suppose we make \(1000\) per month payments at prime minus various amounts. At the end of a 5 year (60 month) term, we have the following future values

With a mortgage amount of 225K and the nominal monthly payment amount of 1K, is this negotiation worth the time? It appears that finding somebody willing to loan at prime minus 0.6% vs. prime minus 0.5% is only worth about $550 after five years. That saving amounts to about 1.5 months of the banks interest profit.

It’s interesting to see that, despite the bank making on the order of 25K for such a mortgage after five years, how little they are willing to move in their adjustment of interest rates.

If you have the wolfram CDF plugin installed, equations \ref{eqn:mortgageInterest:120}, and \ref{eqn:mortgageInterest:160} can be executed using the following simple monthly compounding rate calculator app